JEEVAN DEEP (UIN : 512N270V01)

The Life Insurance Corporation (LIC) of India local division launched a micro insurance policy called ‘Jeevan Deep T-810’ for the benefit of the common man on the occasion of its 56 anniversary on Saturday. The idea is to reach out to the economically weaker sections through the micro-policy. Addressing a press conference on the occasion on the office premises here on Saturday, LIC Senior Divisional Manager D. Tandi said that the insurance product was launched nationwide.

This is an endowment assurance with an added feature of guaranteed additions along with provision of loyalty addition. An immediate annuity product is available for ‘online buy’. Policyholders in the age group of 18 to 60 are eligible for insurance coverage. The policy term is 5 to 15 years. The minimum insurance coverage is Rs.5,000 and the maximum is Rs.30,000. Those who pay the premium amount without fail for two years will have complete insurance cover for the next two years.

Product Summary:

It is a simple savings related life insurance plan with Guaranteed Additions where you may pay premiums either in lumpsum or regularly at monthly, quarterly, half-yearly or yearly intervals over the term of the policy.

1. Sample Premium Rates:

Following are some of the sample premium rates per Rs 1000/- Basic Sum Assured:

Annual Premium ( in Rs.) for Rs 1000/- Basic Sum Assured:

Age (yrs.) | Term of the Policy (years) |

5 | 10 | 15 |

20 | 210.60 | 107.30 | 70.25 |

30 | 210.70 | 107.45 | 70.55 |

40 | 211.3 | 108.45 | 71.95 |

50 | 213.45 | 111.75 | 76.30 |

Single Premium ( in Rs.) for Rs 1000/- Sum Assured

Age (yrs.) | Term of the Policy (years) |

5 | 10 | 15 |

20 | 923.65 | 789.45 | 679.85 |

30 | 923.70 | 789.75 | 680.85 |

40 | 924.10 | 791.80 | 686.15 |

50 | 925.50 | 798.35 | 701.50 |

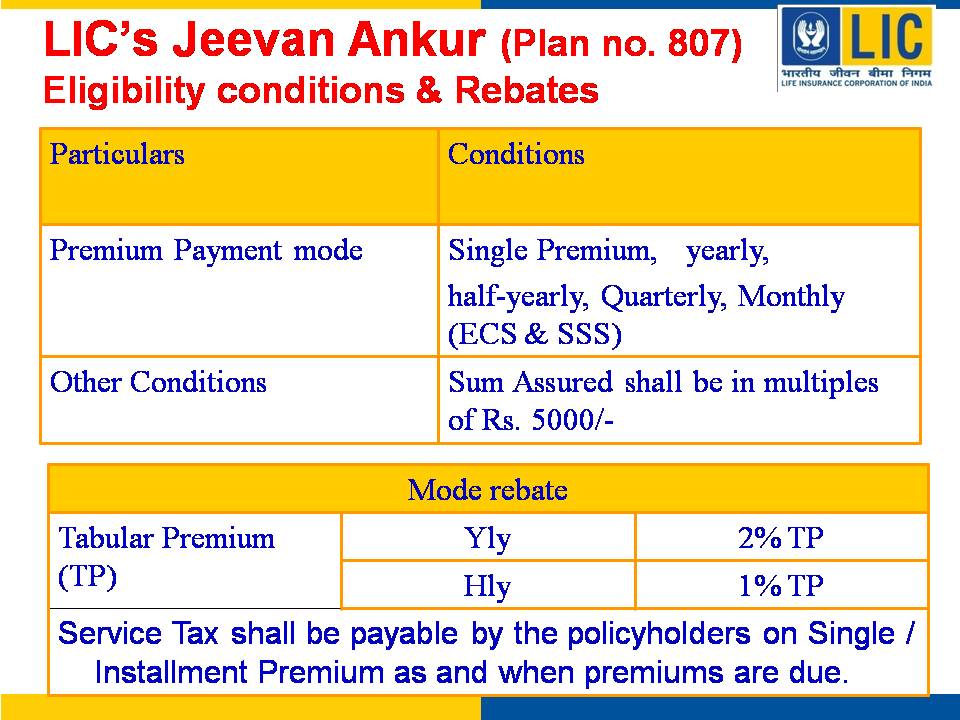

2. Eligibility Conditions and Other Restrictions:

Minimum age at entry : 18 years (completed)

Maximum age at entry : 60 years (nearest birthday)

Maximum Maturity Age : 65 years (nearest birthday)

Policy Term : 5 to 15 years

Minimum Sum Assured : Rs. 5000/-

Maximum Sum Assured : Rs. 30000/-

Sum Assured shall be in multiples of Rs. 1,000/-

3. Grace Period: A grace period of two calendar month but not less than 60 days will be allowed for all modes of payments.

4. Revival: Under regular premium policies, if premiums are not paid within the grace period the policy will lapse. Subject to production of satisfactory evidence of continued insurability, a lapsed policy can be revived by paying arrears of premium together with interest within a period of five years but before maturity from the due date of first unpaid premium. The rate of interest applicable will be as fixed by the Corporation from time to time.

5. Nomination: As per Section 39 of Insurance Act, 1938.

6. Cooling-off period: If you are not satisfied with the Terms and Conditions of the policy you may return the policy to the Corporation within 15 days from the date of receipt of the policy bond stating the reason of objections. On receipt of the same the Corporation shall cancel the policy and return the amount of premium paid after deducting the proportionate risk premium and stamp duty.

7. Exclusions: This policy shall be void if the Life assured (whether sane or insane at the time) commits suicide at any time within one year from the date of commencement of risk and the Corporation will not entertain any claim under this policy except to the extent of a maximum of (i) 90% of the single premium paid excluding any extra premium paid or (ii) third partys bonafide beneficial interest acquired in the policy for valuable consideration (but limited to the basic sum assured of this policy) of which notice has been given in writing to the branch where the Policy is being presently serviced (where the policy records are kept) at least one calendar month prior to death.

Illustration:

Notes :i) This illustration is applicable to a non-smoker male/female standard (from medical, life style and occupation point of view) life.ii) The non-guaranteed benefits (1) and (2) in above illustration are calculated so that they are consistent with the Projected Investment Rate of Return assumption of 6% p.a.(Scenario 1) and 10% p.a. (Scenario 2) respectively. In other words, in preparing this benefit illustration, it is assumed that the Projected Investment Rate of Return that LICI will be able to earn throughout the term of the policy will be 6% p.a. or 10% p.a., as the case may be. The Projected Investment Rate of Return isnot guaranteed.iii) The main objective of the illustration is that the client is able to appreciate the features of the product and the flow of benefits in different circumstances with some level of quantification. iv) The Maturity Benefit is the amount shown at the end of the policy term

Benefits

1. Death Benefit:

On death during the policy term excluding last policy year: Basic Sum Assured along with accrued Guaranteed Additions.

On death during last policy year : Basic Sum Assured with accrued Guaranteed Additions along with Loyalty Addition, if any.

Maturity Benefit:

On surviving to the date of maturity, payment of the Basic Sum Assured along with accrued Guaranteed Additions and Loyalty Additions, if any, shall be payable

Guaranteed Addition:

The policy provides for Guaranteed Addition of Rs 20/- per Rs.1000/- Basic Sum Assured per year during the term of the policy.

Loyalty Addition:

Depending upon the Corporations experience,the policy shall be eligible for Loyalty Addition during the last year of the policy at such rate and on such terms as may be declared by the Corporation.

2. Optional Rider:

Accident Benefit Rider : Accident Benefit Rider Option will be available under the plan by the payment of additional premium. This option is available under Regular Premium policies only.

In case of accidental death, the Accident Benefit Sum Assured will be payable as lump sum along with the death benefit under the Basic plan. In case of accidental disability, an amount equal to the Accident Benefit Sum Assured will be paid in monthly instalments spread over 10 years or up to death or maturity, if earlier, and all future premiums under the policy will be waived.

If the policy becomes a claim either by way of death or maturity before the expiry of the said period of 10 years, the disability benefit instalments which have not fallen due will be paid along with the claim.

3. Auto-Cover Facility:

If at least two full years premiums have been paid in respect of this policy, any subsequent premium be not duly paid, full death cover shall continue from the due date of First Unpaid Premium (FUP) for a period of two years or till the end of policy term, whichever is earlier.

During the Auto Cover Period, the Accident Benefits shall not be available.

4. Paid-up Value:

Under regular premium policies, if after at least two full years premiums have been paid in respect of this policy, any subsequent premium be not duly paid, this policy shall not be wholly void, but shall subsist as a paid up policy. The Basic Sum Assured under the policy shall be reduced to such a sum, called Paid-up Sum Assured, as shall bear the same ratio to the Basic Sum Assured as the number of premiums actually paid bears to the total number of premiums originally stipulated for in the policy.

This paid up sum assured along with accrued Guaranteed Additions shall be payable on the date of maturity or on Life Assureds prior death after the expiry of Auto Cover period.

Accident Benefit Rider will cease to apply if the policy is in lapsed condition.

5. Surrender Value:

The Guaranteed Surrender Value is as under:

For Regular Premium policies - The Guaranteed surrender value will be available after completion of two policy years and at least two years premiums have been paid and is equal to 30 % of the premiums paid excluding the premium paid for the first year and all premiums in respect of Accident Benefit rider and extras, if any.

For Single Premium policies- The Guaranteed Surrender Value will be available after completion of at least one policy year and is equal to 90 % of the premium paid excluding extra premium, if any.

The cash value of accrued Guaranteed Additions will also be payable.

Corporation may, however, pay special surrender value as the discounted value of Paid up Sum Assured and accrued Guaranteed Additions provided the same is higher than Guaranteed Surrender Value.

6. Loan: No loan facility is available under this plan.

7. Cooling-off period: If you are not satisfied with the Terms and Conditions of the policy you may return the policy to the Corporation within 15 days from the date of receipt of the policy bond stating the reason of objections. On receipt of the same the Corporation shall cancel the policy and return the amount of premium paid after deducting the proportionate risk premium and stamp duty.